Condo Operations

Reserve Funds

A reserve fund is an account that condominium corporations maintain solely for major repairs and replacements of common elements and assets. The Condo Act requires that corporations conduct periodic reserve fund studies to determine whether the amount of money in the fund and contributions collected from owners are adequate and can sustain expected costs of major repair and replacement of the common elements and assets.

Understanding Reserve Fund Studies

Reserve Fund Studies can only provide an estimate of future costs. They are similar to a homeowner’s plan for saving for keeping their home in good repair. Importantly, studies must be completed by qualified professionals with expertise in this area.

Contents of a Reserve Fund Study

Reserve fund studies are very important and have specific content requirements under the Condo Act and its associated regulations. Reserve fund studies will typically include:

1. Physical analysis – an assessment of the corporation’s component inventory including year of acquisition, remaining life, estimated cost of replacement, etc. for each item.

2. Financial analysis – an assessment of the financial health of the reserve fund that must include a description of the financial status of the reserve fund as of the date of the study, a recommended funding plan projected over a period of at least 30 consecutive years, etc.

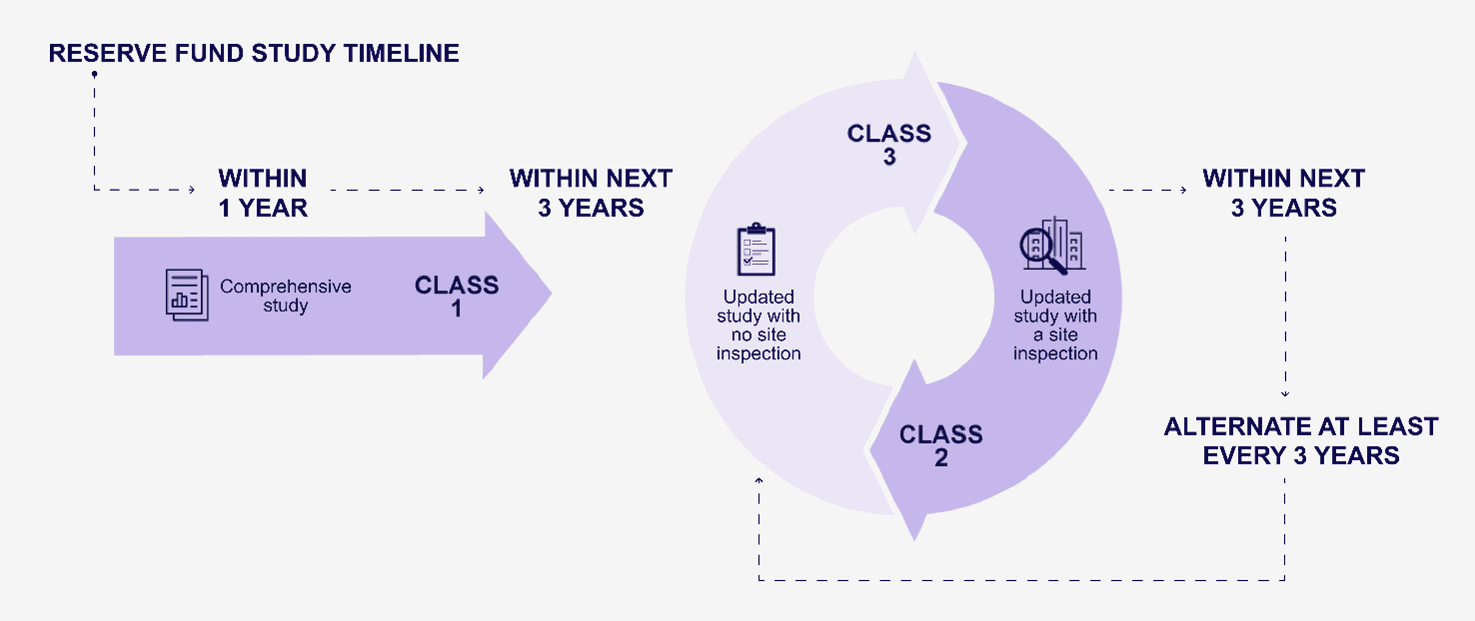

Types and Timing of Reserve Fund Studies

There are three types of reserve fund studies:

A condo corporation must complete a class 1 study within the first year following the registration of the declaration and description. After the first class 1 study is done, the class 3 and class 2 studies are done on an alternating basis at least every three years as seen below:

Plans for Future Funding

Condo boards must review the reserve fund study within 120 days of receiving it and propose a plan for future adequate funding.

The plan must ensure that the fund is adequate by the fiscal year after the study was completed. This may require that boards increase contributions to the fund.

Boards must decide how much to contribute to the fund and should be cautious if choosing to deviate from professional advice. Ignoring this advice could lead to liability issues for directors.

Notice of Future Funding

Boards must send owners a notice of future funding within 15 days of proposing a plan. The notice must contain:

- A summary of the reserve fund study

- A summary of the proposed plan for future funding

- A statement indicating the areas, if any, in which the proposed plan for future funding differs from the reserve fund study

This notice is not an ad hoc document created by the condo board, but rather a specific form that the condo corporation is required to use under the Condo Act.

The board must also send the corporation’s auditor copies of the reserve fund study, the proposed plan for future funding and the notice that was sent to owners. After this is complete, board must implement the proposed plan 30 days from the date on which they sent the plan to the owners and the auditor.